If you have been trying to understand mutual fund indexation, you are not alone. The term sounds technical at first, but the idea is actually simple once you break it down. In India, mutual fund indexation was once one of the biggest tax advantages for long term debt fund investors, so it still matters if you want to understand older investments and current tax planning.

In India, mutual fund indexation means increasing your purchase cost with the Cost Inflation Index, so inflation reduces your taxable long term capital gain. However, this benefit no longer applies to most debt mutual funds bought on or after 1 April 2023, and long term gains taxable under Section 112 on transfers from 23 July 2024 are generally taxed at 12.5 percent without indexation. So today, mutual fund indexation mostly matters when you review older debt fund holdings, past redemptions, or legacy tax planning.

Why this topic still matters

Many people hear that indexation is gone and stop there. That creates confusion, because some investors still hold older debt mutual funds, some people are checking past redemptions, and others are comparing debt funds with fixed deposits, bonds, or hybrid funds. In other words, the keyword still gets searched because investors want clarity, not tax jargon.

This is also where many articles fail readers. They explain the old rule, but they do not explain what changed, who was affected, and what investors should do next. A useful guide should help you understand the past rule, the current rule, and the practical decision you need to make today.

What is mutual fund indexation

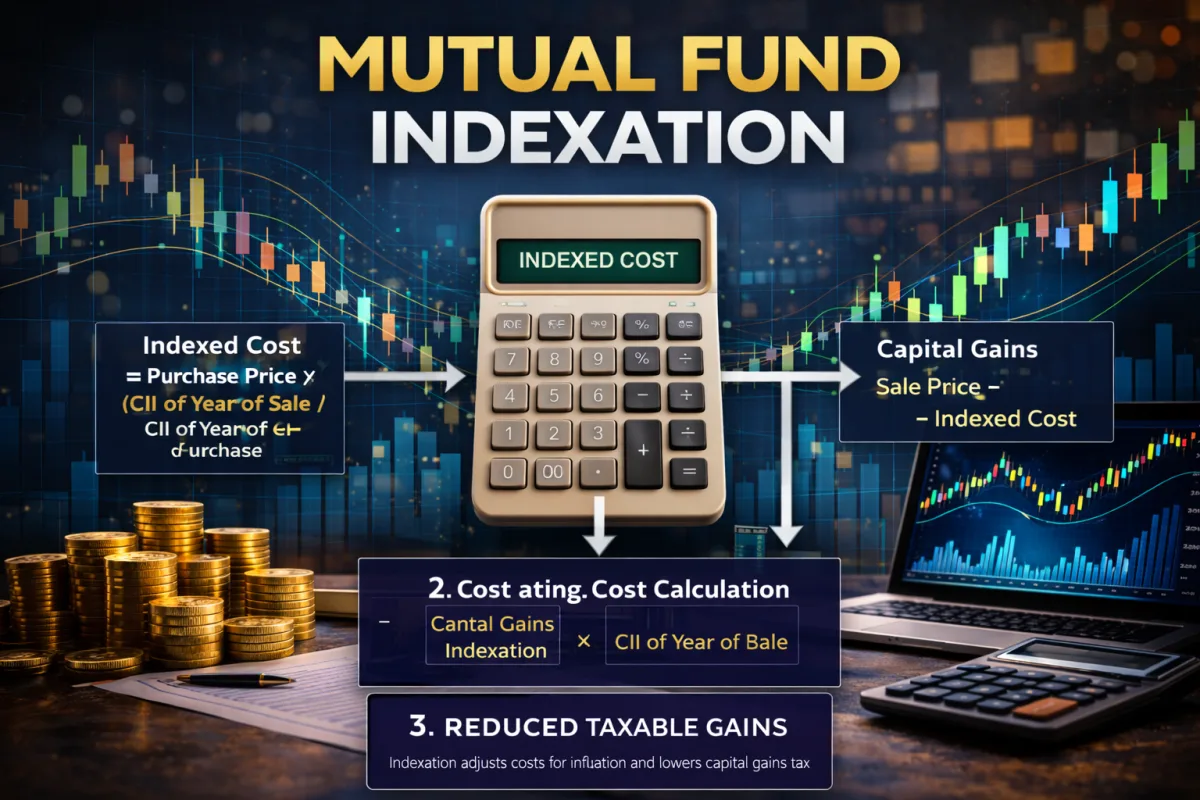

Mutual fund indexation is a tax method that adjusts your purchase price for inflation. Instead of taxing the full gap between buying price and selling price, the law first increases your cost using the Cost Inflation Index, also called CII. That higher cost reduces the taxable gain.

Think of it this way. If prices in the economy went up while you held an investment, part of your gain may only reflect inflation, not real wealth creation. Indexation tried to account for that inflation effect, so tax applied more fairly to the real gain.

This benefit became especially popular with debt mutual funds. Investors who held them for the long term often liked the mix of potentially better post tax returns, steady income style investing, and lower tax outgo compared with fully taxable alternatives.

How mutual fund indexation worked, step by step

The formula was simple in principle. You took your original purchase cost and multiplied it by the Cost Inflation Index of the sale year, then divided it by the Cost Inflation Index of the purchase year. That gave you the indexed cost of acquisition.

After that, you subtracted the indexed cost from the sale value. The result was your taxable long term capital gain. Therefore, the higher the inflation over your holding period, the bigger the indexed cost, and the smaller the taxable gain.

A simple example

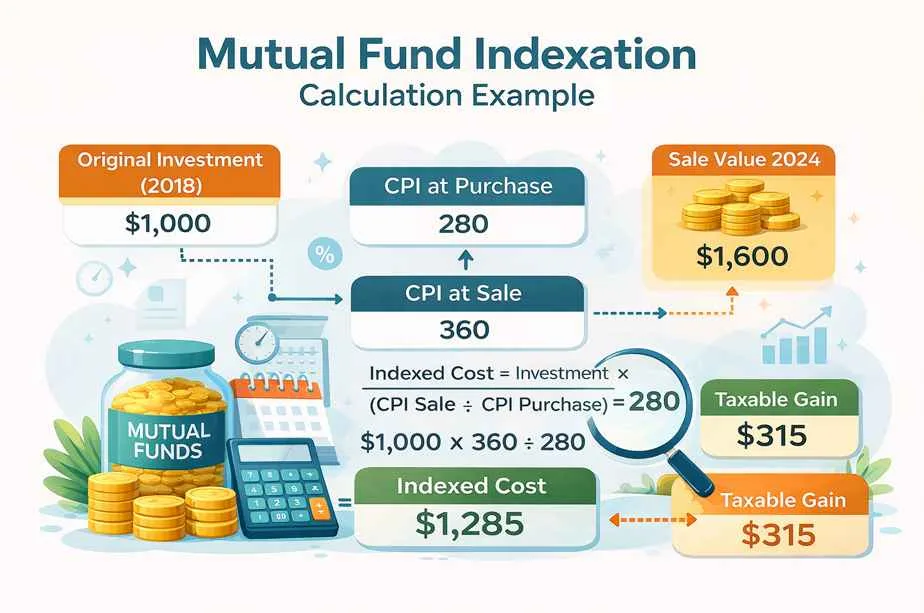

Imagine you invested Rs 1,00,000 in a debt mutual fund years ago. Later, you sold it for Rs 1,40,000. Without indexation, your capital gain looks like Rs 40,000, but with indexation, your adjusted cost may rise enough to cut that taxable gain meaningfully.

That is why investors loved this rule. It rewarded patience, acknowledged inflation, and often reduced the effective tax burden in a very visible way. For long term investors, even a modest reduction in tax could improve net returns in a big way over time.

| Example Item | Without Indexation | With Indexation |

|---|---|---|

| Purchase value | Rs 1,00,000 | Rs 1,00,000 |

| Sale value | Rs 1,40,000 | Rs 1,40,000 |

| Inflation adjusted cost | Not used | Example, Rs 1,18,000 |

| Taxable gain | Rs 40,000 | Rs 22,000 |

What changed in the tax rules

This is the section most readers actually need. The old answer to mutual fund indexation was simple, but the current answer depends on when you bought the fund, what kind of fund it is, and when you sold it. Once you know those three things, the confusion starts to clear.

The 1 April 2023 change

For most traditional debt mutual funds bought on or after 1 April 2023, the old long term capital gains benefit with indexation stopped applying. In practical terms, many such gains started getting treated like short term capital gains under the special rule for specified mutual funds. That means they are generally taxed at your slab rate, even if you hold the fund for a long time.

This change was a major turning point. Before it, many investors used debt funds partly because indexation could improve post tax returns. After it, the tax edge of fresh debt fund investments became much weaker for many people.

The 23 July 2024 change

Then came another major shift. For many long term capital gains taxable under Section 112, the tax moved to 12.5 percent without indexation for transfers on or after 23 July 2024. So even some older holdings that once benefited from 20 percent tax with indexation moved into a new system without the inflation adjustment.

This is why many investors feel lost today. They remember that debt fund indexation was a big benefit, which is true, but they are looking at a tax landscape that now works very differently. Therefore, you cannot rely on old advice without checking purchase date and redemption date together.

| Investment Situation | Broad Tax Treatment | Indexation Benefit |

|---|---|---|

| Most debt mutual funds bought on or after 1 April 2023 | Usually taxed like short term capital gains at slab rate | No |

| Older debt fund holdings sold before 23 July 2024, where old long term rules applied | 20 percent on long term gains | Yes |

| Many long term Section 112 cases on transfers from 23 July 2024 | 12.5 percent | No |

| Equity oriented mutual funds | Separate equity capital gains rules apply | No |

Which mutual funds used to get indexation

Indexation was mainly associated with debt mutual funds and some debt heavy hybrid structures. It was never a universal benefit across every mutual fund category. That is one of the biggest misunderstandings readers carry into this topic.

Debt mutual funds

Debt funds were the most common place where investors discussed indexation. These funds invest in bonds, treasury bills, money market instruments, and similar fixed income assets. For years, they were seen as a smart choice for investors who wanted stability plus better post tax efficiency.

Hybrid funds and similar structures

Some hybrid funds could fall into different tax treatment depending on how they were structured. That is why fund classification matters so much. A fund label alone does not tell the full story, and investors should always verify the actual category and tax treatment before assuming indexation applies.

Equity mutual funds

Equity oriented mutual funds do not use indexation for capital gains tax. They follow a different system, with their own holding period and tax rate rules. So if your fund mainly holds equities, the keyword mutual fund indexation usually does not describe your main tax advantage.

Why purchase date matters more than ever

Today, the date you bought the fund can matter more than the return itself when you estimate post tax profit. Two investors can hold similar debt funds, earn similar gains, and still pay different tax because one invested before 1 April 2023 and the other invested later. That is why purchase history is now a core part of tax planning.

The sale date matters too. A redemption before 23 July 2024 could fall under a different long term tax logic than a redemption after that date. So the real answer is not, does this fund have indexation, but rather, what is my purchase date, what is my sale date, and which rule applies to that exact combination.

The real benefit indexation gave investors

The biggest benefit was not just lower tax. It was fairer taxation in an inflationary economy. If inflation quietly raised prices over several years, indexation tried to avoid taxing that inflation as if it were real profit.

It also encouraged long term investing. People who held debt funds for years could feel that patience had a reward. In addition, it made debt mutual funds more attractive in a tax comparison with some traditional fixed income products.

This is why many investors still feel disappointed that the benefit is now limited. They were not only chasing a lower number on a tax form. They were trying to improve real, after tax wealth, which is what smart investing is supposed to focus on.

What mutual fund indexation means in 2026, in plain English

For most fresh debt fund buyers, indexation is no longer the headline benefit it once was. If you buy a typical debt mutual fund now, you should not build your plan around getting indexation. Instead, you should compare expected return, tax slab impact, liquidity, risk, and how the fund fits your goals.

However, the topic is still useful for three groups of people. First, investors reviewing old debt fund units bought before the April 2023 rule change. Second, investors checking how past redemptions were taxed. Third, readers who want to understand why debt funds used to be marketed as tax efficient products.

Common mistakes investors make

Assuming every mutual fund gets indexation

This is the most common error. People hear the phrase mutual fund indexation and assume it applies to all funds. In reality, equity funds follow a different capital gains system, and debt fund rules changed sharply after April 2023.

Ignoring the purchase date

Your purchase date can change the whole answer. Many investors look only at current rules and forget that legacy holdings may follow a different path. That can lead to wrong tax estimates and poor exit decisions.

Ignoring the sale date

The 23 July 2024 change matters because the tax rate structure changed for many long term gains. So even if an investment began under an older system, the actual date of transfer may pull it into a newer rule set. Therefore, old holdings still need fresh review.

Forgetting to compare post tax returns

Some investors compare only gross returns. That is a mistake, because a product with a slightly lower headline return can still leave you with more money after tax. This is where simple comparison work matters, and a clear numbers first approach helps a lot.

Skipping records and statements

You need purchase date, purchase value, sale value, and basic fund details. Without clean records, tax filing gets harder and planning becomes guesswork. A small amount of organization can save a lot of stress later.

Smart planning tips for today

First, choose a fund for the goal, not only for an old tax story. If your goal is emergency liquidity, short term parking, or diversification, a debt fund may still have a role. Just do not assume it has the same tax edge it had a few years ago.

Second, always check the post tax result. A fund that looks strong before tax may look average after tax if you are in a high slab.

Third, keep your calculations simple and honest. If numbers confuse you, build a plain comparison sheet and test different sale values, holding periods, and tax outcomes. The same practical mindset behind a discount value table can help you compare post tax investment results more clearly.

Fourth, avoid mixing long term investing with short term market noise. Debt funds are generally about allocation, stability, and cash flow style goals, not daily excitement. If you want to understand the bigger discipline behind patient investing, this guide on investment style long only hedge fund thinking can help you see why time horizon matters so much.

How to check whether indexation matters in your case

Ask yourself four questions. What kind of mutual fund is it. When did I buy it. When did I sell it, or when will I sell it. Under which capital gains rule does it fall. Once you answer those, the path becomes much easier.

You should also check trustworthy sources when rules change. The Income Tax Department capital gains guide are good starting points because they help you verify the current framework before making a decision.

Should you still invest in debt mutual funds if indexation is gone

Yes, sometimes you should. Debt mutual funds can still help with diversification, liquidity, duration strategy, and access to different bond market segments. A product does not become useless just because one tax benefit changed.

However, you need a more honest framework now. Instead of asking only, will I get indexation, ask, what is my goal, what is the likely post tax return, how much volatility can I handle, and is this better than my other options. That shift in thinking usually leads to better decisions.

Final takeaway

Mutual fund indexation used to be a major reason investors loved debt funds in India. It adjusted cost for inflation, lowered taxable gains, and made long term holding more attractive. Today, that benefit is no longer the main tax story for most new debt mutual fund investments.

The smart move now is simple. Check the fund type, check the purchase date, check the sale date, and compare post tax outcomes before you act. If you review your holdings with those four steps, you will make better decisions and avoid the confusion that traps so many investors.

If you have old debt fund units or are planning a redemption soon, review them carefully now instead of waiting until tax season. A clear decision today can save money, reduce stress, and help you build a more tax aware portfolio.